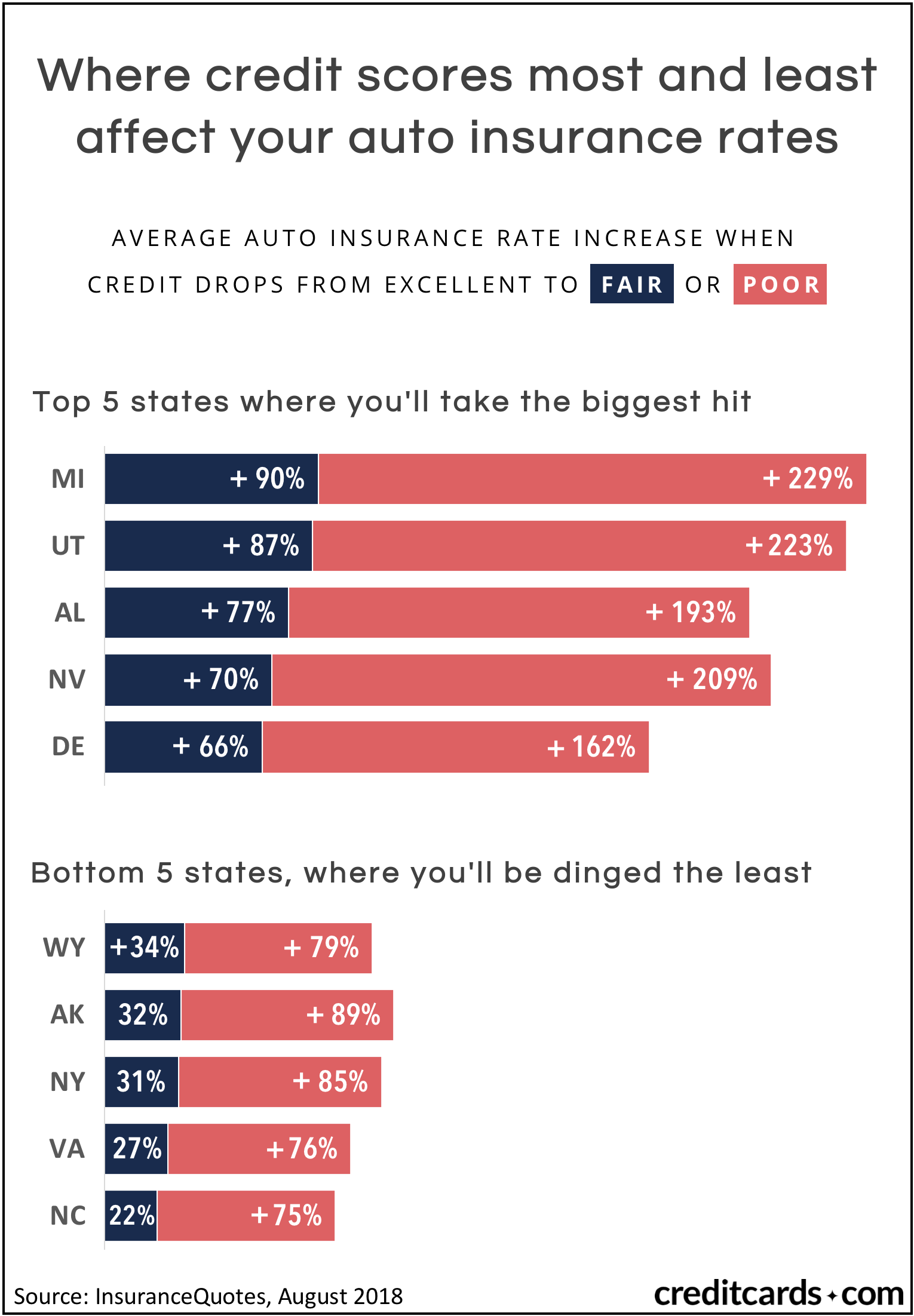

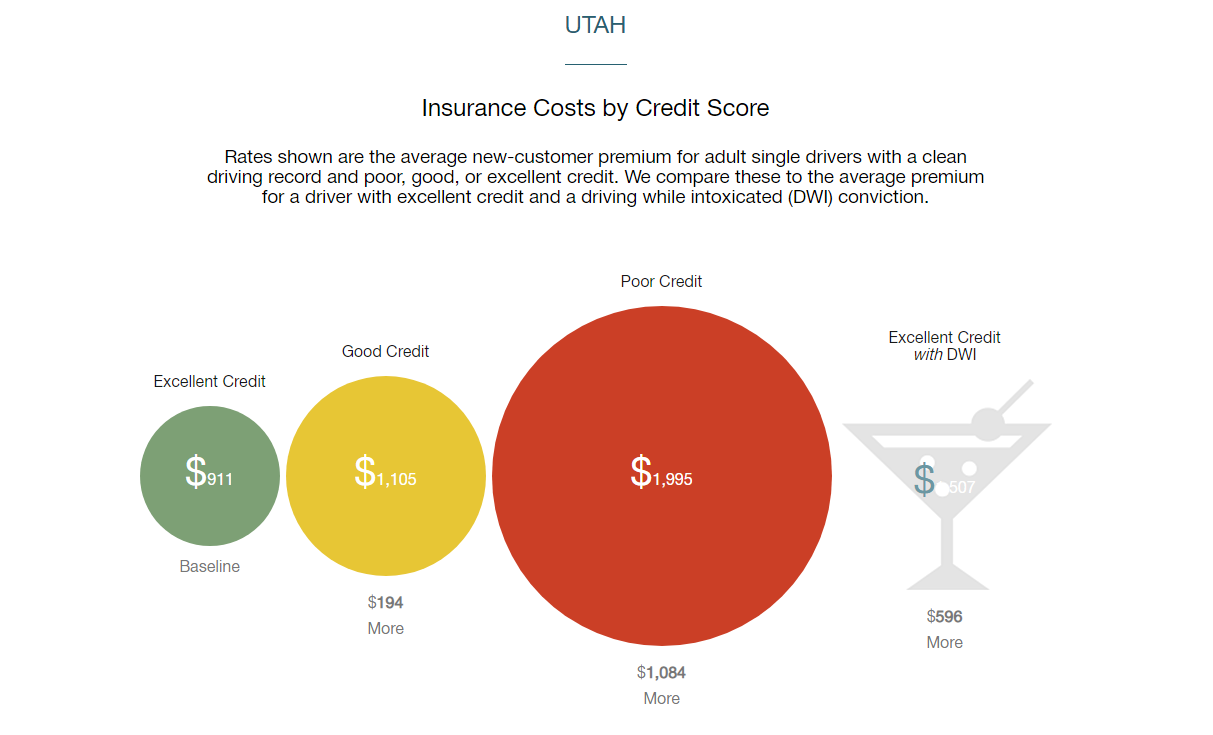

ST. GEORGE — A recent study has ranked Utah as No. 2 in the list of states where consumers with little or bad credit are most effected when it comes to paying for automobile insurance.

A 2018 study commissioned by insuranceQuotes focused on how much annual premiums can change based on one unique factor: the driver’s credit rating.

The study analyzed rates using a hypothetical 45-year-old married female driver with a bachelor’s degree and no prior claims or lapses in coverage.

The findings showed that on average nationally, drivers with fair credit paid 28 percent more than their stellar-credit counterparts, and drivers with bad credit paid double. In Utah, people with bad credit are paying 146 percent more than those with great credit.

Same state, same policy, but the price more than doubles based on that unique factor.

Other factors that determine the cost of coverage — usually to a lesser degree than credit score — include the applicant’s driving record, age, sex and home ownership, as well as marital status, how the driver’s car is used, longevity with the current insurance company and years without incidents.

There are also demographic factors that play a role in pricing, as insurance rates vary from one area or state to another based on the number and cost of claims filed in a particular geographical area. The number of autos in a local area or zip code, traffic congestion and the average number of crashes reported in a particular location also play a role in determining the costs for coverage. These factors are among the reasons auto premiums tend to be higher in metropolitan areas, according to a 2015 Consumer Affairs report.

All that makes sense, but why credit rating?

Using credit score information has been standard practice in the automobile insurance industry for nearly three decades — a practice based on the premise that an individual’s credit score is a credible predictor of how likely they are to file a future claim, according Consumer Affairs.

Studies show that people who manage their finances well tend to also manage other important aspects of their lives responsibly, including driving habits.

St. George News surveyed several agents in Southern Utah, and their answers varied on the importance credit plays in auto insurance pricing.

One of the agents surveyed said driving record has a much greater impact on insurance rates. Another said the credit rating was the No. 1 denominator affecting pricing, adding that even if the credit score falls by one point, the rate is affected.

More than one agent said they also look at how long an applicant has been with their previous car insurance company; if an applicant changes insurance companies often, it can be a sign of a poor payment history.

In some cases, an individual buys a policy to show proof of insurance, lapses their monthly payment and then continues the cycle of stopped payments with a new policy.

Insurance companies began using credit scores to determine a premium amount in the 1990s. By 2006 nearly every insurer was using them to set prices and pull a soft credit inquiry, which can only be seen by the individual and does not lower the credit score.

The advancement of information technology has led to the development of the “credit-based insurance score,” a numerical ranking system based on a person’s credit payment history and other factors used to help underwriters charge a premium equal to the risk they are assuming.

However, the use of credit-based insurance scores is banned in three states: California, Hawaii and Massachusetts. According to the Consumer Affairs report, in these states, the price of car insurance is based mainly on “how people actually drive and other factors, not some future risk that a credit score predicts.”

Many consumers aren’t even aware that their credit history is factored into auto insurance pricing, according to a 2016 survey commissioned by insuranceQuotes.

Further, insurance companies are under no legal obligation to show policy holders their credit-based insurance score.

One of the agents surveyed by St. George News refuted the notion that a person’s credit score is released to the agent and said it is illegal in Utah to pull an applicant’s credit report.

But that’s not the case according to the Utah Insurance Department, a state agency that sets defined parameters in terms of how much an insurance company can charge for coverage to protect the consumer from exorbitant insurance rates.

According to the department’s website, an applicant’s credit score can in fact be used to determine the cost for coverage under the Fair Credit Reporting Act, a federal law that says insurance companies have a “permissible purpose” to look at an individual’s credit information “without their permission.”

However, Utah law prohibits insurers from relying solely on credit-based information to raise premiums or to deny, cancel or refuse to renew a policy.

Most insurance companies use an insurance score, the state agency said, which is a snapshot of that person’s credit at a moment in time, as well as other factors. The list of common credit factors used in determining insurance scores is as follows:

- Major negative items: bankruptcy, collections, foreclosures, liens, charge-offs, et cetera.

- Past payment history: number and frequency of late payments, days elapsed between due date and late payment date.

- Length of credit history.

- Homeownership.

- Inquiries for credit.

- Number of credit lines open.

- Type of credit in use.

- Amount of outstanding debt.

One side effect to allowing credit scores to be used to set pricing in auto policies is that it essentially forces the consumer to pay for accidents that haven’t happened and may never happen. Further, it undermines the ability for low-income drivers to get insurance because it drives the cost up for those who can least afford it.

“For some customers, there has been a cataclysmic event that lowered their credit score, but that doesn’t mean they are a risk. But the rate goes up regardless,” one of the surveyed agents said.

Taxing the poor through credit scoring and by other means not related to driving causes problems for all insured drivers because painfully high insurance prices tempt financially strapped consumers to drive without insurance, which is supported by the fact that there are 30 million uninsured drivers nationwide, according to the Insurance Research Council.

The goal of an insurance company is to match insurance policy rates with the actual costs of claims as accurately as possible. If one company’s rates are too high, they have essentially priced themselves out of the market, leaving their share to competitors more skilled in matching rates with anticipated claim costs at a higher degree of accuracy. Setting rates too low, the company loses money and is out of business.

This ongoing pursuit for balance is designed to protect low-risk consumers from paying for those who pose a higher insurance risk, but according to Consumer Affairs, there are ways for individuals to improve their credit-based insurance score while also improving their overall credit score. Most importantly, make all credit payments on time, don’t open new credit accounts unless absolutely necessary and keep credit card balances as low as possible.

Certain types of credit that insurance company credit-scoring models penalize for should be avoided, including department store credit cards, instant credit offered by stores to move big-ticket items and finance company cards.

Drivers should keep track of their consumer credit score and make sure their insurance policy also reflects any positive changes over the years. One of the surveyed agents said most carriers will run credit scores upon request, which can help lower premium costs.

Email: [email protected]

Twitter: @STGnews

Copyright St. George News, SaintGeorgeUtah.com LLC, 2018, all rights reserved.

“Studies show that people who manage their finances well tend to also manage other important aspects of their lives responsibly, including driving habits.” That pretty much says it all. Being poor and having a bad credit score do not go hand in hand.

agree 100%

“Further, it undermines the ability for low-income drivers to get insurance because it drives the cost up for those who can least afford it.”

Being poor doesn’t mean you have bad credit. Conflating the two is being wilfully dishonest with facts.

I am an insurance agent and totally disagree with using credit as a determining factor in a insurance rate. I know many many people that make $7 to $10 an hour. They have perfectly clean driving records, yet because they are poor and trying to raise a kid, and pay rent, utilities, buy groceries, on and on, their credit suffers. It is so completely unfair to make them pay more because they are the unfortunate. Some people cant afford college so that they can get good jobs. This country is so backwards and make the poor and middle class pay for the previledged, with the good credit scores. Regardless of their driving record. I have been a insurance agent for 40 years, and was when this went in to force. I have totally disagreed with it from day one. And yes if the poor have to choose between feeding their child, or paying insurance i would hope they would feed their children.

You say that till you get t-boned when they blow a stop sign and don’t have insurance. You say you’ve been an insurance agent for 40 years, bet you have benefited financially from this policy, although you don’t like it.

People can be poor and have good credit scores.

I have also been in the business forever, and am completely in favor. The data absolutely backs up the fact that those with the worst consumer scores submit far more claims, costing a lot more money than those with higher consumer scores. People ask “what does my credit have to do with my driving?” But it turns out that is the wrong question. The relevant question is “how does my credit predict my propensity to submit claims?”

Insurance companies are not charities. They have to use premiums to pay claims. Regulators are there to make sure they charge adequate premiums to have the money to pay those claims. Over 20 years ago, one state’s legislature commissioned its flagship university to do a study to prove credit scoring was irrelevant. The university came back after the study and said that credit scoring was a far better predictor of claims than driving record. When insurers started using credit scoring to make rates, one very large insurance company held back, thinking it seemed unfair. They were giving their best rate to everyone with a clean driving record, while competitors were giving their best rate to people with good consumer scores. The result was that the drivers with the best scores (who had almost no claims) left to get better rates at other companies. The drivers with clean records and bad consumer scores stayed, had claims that were 3 times their premiums, and referred all their friends. Within 2 years, that company’s losses wiped out half of their net worth.

For what it’s worth, the most visible person to come out early and advocate for this was Warren Buffet. The use of consumer scoring was what really kicked GEICO into top gear for him.